By Taposh Ghosh

The 21st century has been dubbed ‘the era of disruptions’ with new technologies and innovations penetrating our everyday lives and changing consumer behavior. Consumers are more aware than ever before, holding high expectations from the services they receive. This trend has compelled numerous global industries to look back and rethink about the way they carry out their activities. Emulating the pace, banks and financial institutions also need to reshape and retool to survive and thrive in such challenging times.

Growth for retail banks and other financial institutions has remained illusory in recent years, with organizations experiencing a difficult time saddling their cost of operations. Previously, an average customer was said to interact at least twice a day with their banks to perform some sort of transactional activity; a figure which has been on the decline in recent times. Despite financial services still remaining highly transactional, the current generation of banking customers portrays greater expectations in services and value.

The digital natives seek an enhanced customer experience, reduction in friction, and increase in speed and transparency. This trait of consumer behavior can be traced back to the accepted forms of technology used on a regular basis, e.g. Google and Apple. The retail bank’s attempt to acquire customers in the digital space through mobile applications and online banking are deemed sufficient by most institutions. However, the lack of sophistication and clever use of available technology has created a discontinuity and disconnect between modern customers and their banks.

It does not take a financial expert to deduce that digitization is challenging the very way in which banks operate, with customers not responding well to its slow-shifting legacy models. Yet, digitization also represents significant opportunities for the retail banking industry. The winning strategy lies in integrating technology with existing models and creatively implementing tools and techniques we already have; the pace of which is rapidly intensifying.

Use of Cognitive Banking to Provide a Richer Consumer Experience

The new generation of customers expects their banks to play a more advisory role when it comes to managing their money and making investment decisions; a service which was seldom conducted by traditional banks. But in order to retain and cater to the demands of these digital natives, banks need to gear up and adopt cognitive approaches for better customer support and investment advisory.

Traditional bankers may disagree with the importance of consumer experience in the business. However, the magnitude to which user experience is a concern is spelled out in 2015’s World Retail Banking Report which stated that positive consumer experience had fallen for the second year in a row. The Generation-Y bank customers, unlike their parents, are less likely to stay loyal to their banks. They demand full control over where and how their money is managed and invested, and a cognitive approach can help banks achieve such feats.

So, what is cognitive banking? A bank which has adopted cognitive methods can be termed as a bank which ‘thinks’. The process includes data analytics and machine learning to understand consumer behavioral patterns and produce personalized services. Being one of the most data-intensive industries, the banking industry has the greatest potential in benefitting from cognitive technology to improve their operations and services. More likely than not, the use of deposit slips and cheques are still going to prevail, and the industry will keep on accumulating data, which is no less in value than a currency in today’s world.

To cater to the needs of its younger customers, banks need to leverage its data and act as identity brokers. They should concentrate on tailoring personalized products and services based on advanced customer profiling. In simpler words, banks need to pick up the digital clues their customers leave behind and use them to truly understand what these customers desire from their banking services and ultimately cater to these personalized needs.

Penetration of the Mobile and Digital Payment Market

Payments and completion of monetary transactions have forever been the beachhead for the banking industry. However, new players in the form of Fintech startups are threatening this space. To accommodate the increase in the number of smartphone users and the exponential growth in online activity, these businesses are providing payment gateways and other diverse tools through the use of cellphones, tablets, computers, and so on; these activities are devouring a great chunk of the potential revenue that banks could have acquired.

Many high street banks have already begun to reach customer communities deploying their own mobile payment channels. Nevertheless, for the most part, non-bank players, such as telecommunication companies and small Fintech firms, who are spelling out the standards for digital banking. The average bank’s futile attempts at countering this threat through mobile applications are only limiting users to checking their balances, transactions and transfers.

The secret to the success of these non-bank challengers lie within their size and agility of operations. They are functionally designed for continuous improvement and launch out updates at real time, something which counters the rigidity of banks. The narrow focus on their value-added services helps these competitors cater better to the needs of the fast-paced generation; for example services like PayPal allow merchants to receive payments within one day, almost a couple days faster than most banks.

Banks now need to utilize their already established transactional infrastructures to take over the mobile payment channel. Bkash in Bangladesh is one of the most successful examples that can be highlighted, where a retail bank has redefined mobile payment. These channels help to multiply customer interactions and extend the banks’ commercial footprint through generations of transaction fees.

Valuable insight of the consumer’s future decision can be provided by leveraging on the bank’s pool of raw behavioral data. The key is to use the data strength to create personalized services along the entirety of the consumer decision journey, ultimately aiming to manage the consumers’ entire digital wallet. This extension of value proposition through data can help banks double the revenue earned through mobile and digital channels, and beating the non-bank competitors at their own game.

The Changing Legacy Business Model for Banks

The business model for banks have experienced very insignificant changes entering the 21st century, with the adoption of 24/7 online banking being one of the more crucial ones. But in this era, if the banks do not take the initiative to disrupt themselves, someone else is going to enter the space and take the industry by storm. The insurgence of technology firms such as Google, Apple, PayPal, etc. into the payment arena cries out for the need of traditional financial institutions to sit and look back at their slow-paced business models, if they wish to survive through the upcoming decades.

To take complete advantage of the digital revolution, the banks of the future must provide a comprehensive digital platform to provide for all possible financial services. This has to reflect throughout the entire organization, from front-end commercial activities to back-end technology and operations. Going digital also provides the scope to automate processes – taking an activity which is now done manually, meaning in an error-prone manner, and transforming it into a process which delivers the exact same result every single time. This enables banks to cut off major parts of the cost structure and achieve greater efficiencies.

Personalized consumer experience will be of utmost importance, as use of data strength can lead to introduction of new diverse services targeted towards underserved segments, including small and informal merchants, international travelers, migrant workers, youth market, etc., which can help to channel these customers under the banking umbrella.

Key performance indicators will also need to change, with greater budgets dedicated to digital marketing and decreasing importance on bank branches. Branches will no longer describe the reach and spread of a bank, rather it will act as a consumer touch point when they feel the need for consultancy or a more personalized service. Efficiency ratios will also be pushed into the high 30s and low 40s, as integration of technology will cut down costs.

Embracing the Digital Revolution

We are currently living in a time where innovation is an everyday phenomena and adapting to such changes is the key to survival. With the exponential rise in online commercial activities, banks have crucial roles to play in offering the most secure payment channels and catering services which best suits the consumers. Implementation of cognitive banking and machine learning will open limitless possibilities for banks while satisfying the young consumers’ need for personalized user experiences. Banking in the future is predicted to act as an open ecosystem, where one bank account holds the potential to serve for all of the consumers’ financial needs, both on and off the digital space.

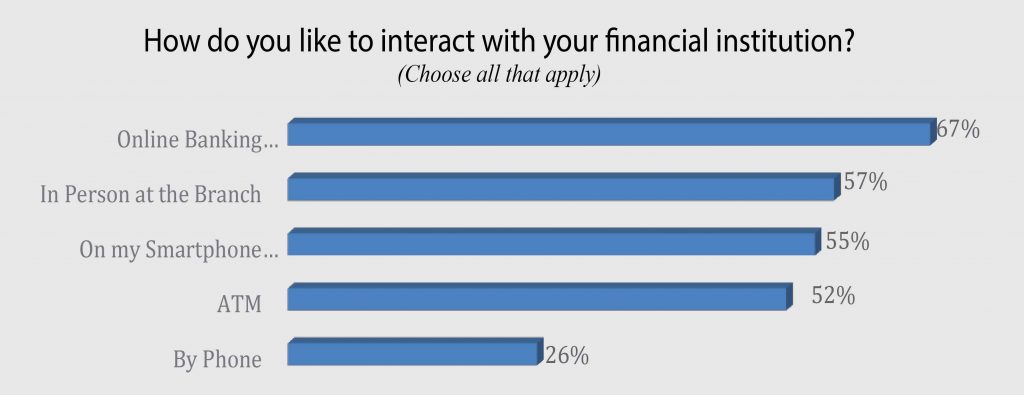

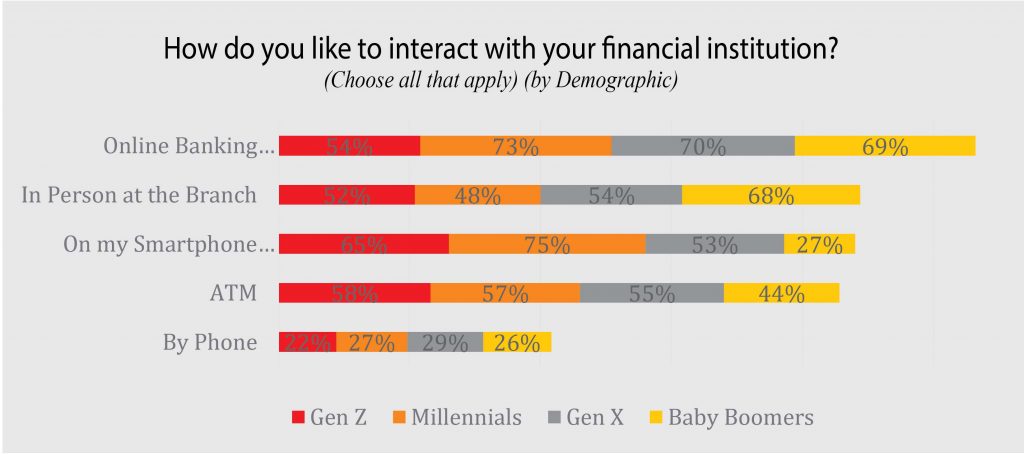

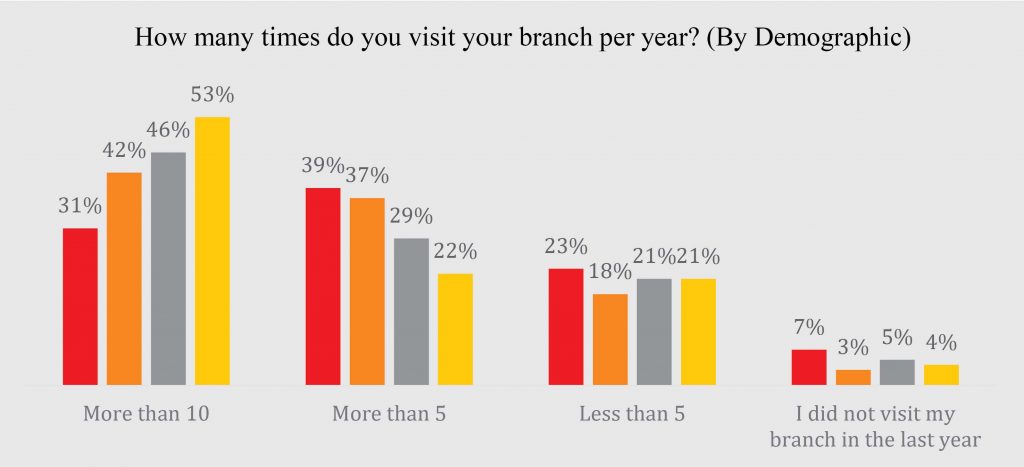

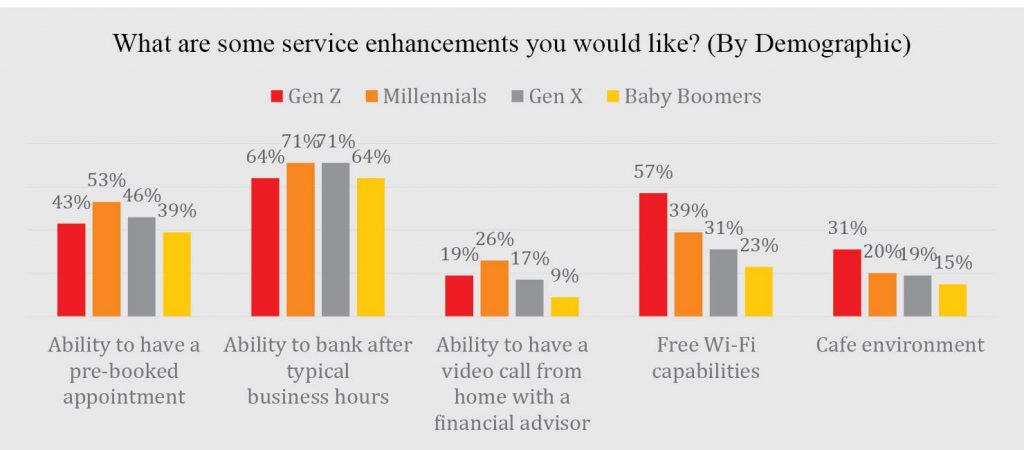

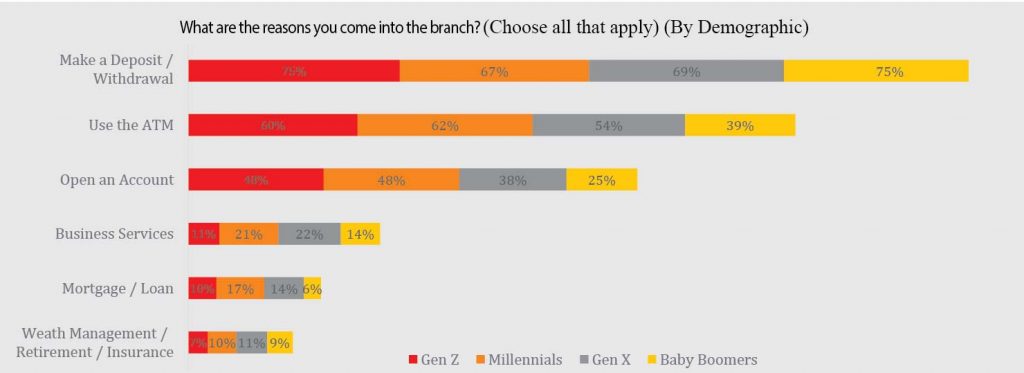

Figures courtesy of ‘The State of Retail Banking Survey 2016’ (online version) from www.timetrade.com