“We are chasing the SME owners to rate them, to help them become bankable”

BDRAL is an initiative of Dun & Bradstreet (D&B) South Asia Middle East Ltd, located in Dubai. Established in 1841, D&B is the world’s leading provider of business information, knowledge and insight

What kind of companies BDRAL rating right at the moment?

We are licensed to rate the small and medium enterprises. Therefore, our ratings are limited to SMEs only at this time. From the government’s part we deal with Bangladesh Securities and Exchange Commission (BSEC) that has given us the license. From Bangladesh Bank’s part, we are an External Credit Assessment Institution (ECAI). These are the two regulators we are working with.

You are working with SME. What kind of ratings do you give them?

Our slogan is “Making SME’s Bankable”. We are chasing the SME owners to rate them to make them bankable, because most of them are not eligible for banking services; especially when it comes to getting loans. We help those who did not qualify for banking services on many grounds. We are glad that Bangladesh Bank is also promoting the idea and trying to bring these SMEs under the umbrella of formal financial services.

How do you rate these companies? Is it based of what kind of business they are doing or what kind of achievements they have made?

Our rating starts from a bank. When an enterprise goes to a bank for loan, the latter would like to rate this new client before sanctioning the loan. After they send us a request, we sign the agreement with the client (the enterprise seeking loan) and then the whole process begins. Our Field Analysts them go to the location of the business and collect and verify the required data. We have a questionnaire which needs to be filled and signed by the client. After collecting all documents from both the client and the requesting bank, we send these files to our Rating team. They do the analysis and give the best judgments and produce the report which has financial data of the business, personal data of the owner, information about the type and condition of business, etc. So, to make it short, we work as a third party for banks to provide data on a particular company. Banks have their own analysis and when we provide them the report, they compare their data with that of ours and finally make a judgment call on whether that particular company should be granted the loan or not.

Do you recommend giving loans?

We don’t. We only provide suggestions. We show the magnitude of risk involved for a bank with the sanctioning of loan to a company.

What BDRAL and D&B are connected? Please enlighten us.

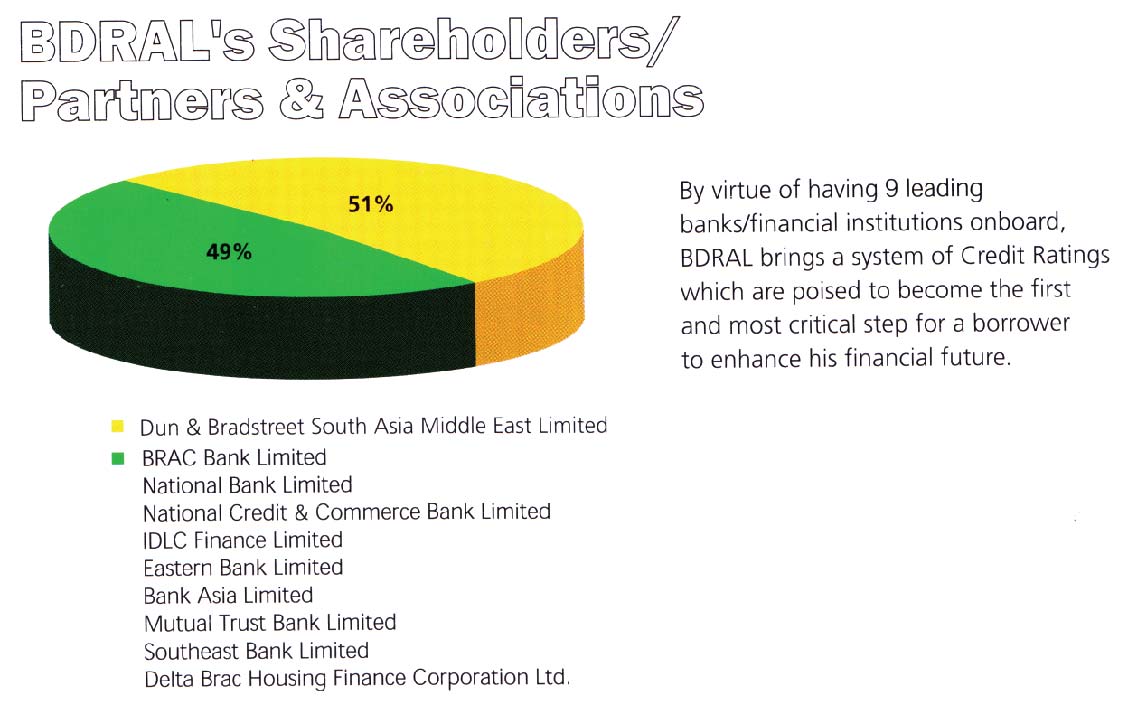

BDRAL is an initiative of Dun & Bradstreet South Asia Middle East Ltd (DBSAME), located in Dubai, UAE and an affiliate of the D&B in the USA. Established in 1841, D&B is the world’s leading provider of business information, knowledge and insight. D&B has been enabling business communities, regulatory authorities and governments across the globe to decide with confidence for 165 years. DBSAME holds 57% of the total share of BDRAL. Though it is not directly involved here in Bangladesh, as a subsidiary we are doing own rating business. In addition, we are working as a correspondent in their data collection activity. We do the business intelligence reporting part for them, where we collect data they need, and report to them and get paid for.

What’s your take on the SME scenario of Bangladesh? Due to political turmoil, they were hit hard.

We live in a country where avoiding political uncertainties is not an option. It has become a part of life and brings along suffering with it for both common people and businesses alike. In ours, SMEs are coming from different backgrounds and venturing into various kinds of business. It’s interesting to collect information about businesses, which many of us even never heard of. Being a part of the rating committee, when I look into those reports, at times I am also quite amazed to see the diversified array of business choices people have made. For instance, I didn’t know that there was a business that collect the trashed plastic bottles (transparent ones), cut them into pieces and re-export to neighboring countries. Even that business has faced some good competitions in recent times. We try to identify if this kind of competitions are unfair or too stiff for businesses to sustain.

Do you have any suggestions for businesses facing tough competitions?

It could have been a part of our consulting services, which right at the moment is not a part of our portfolio. We are thinking of proposing to our parent company and the regulators about whether we could do it. Probably we will render that kind of service in future.

How many banks are you working with? Do you work with both public and private sector?

The estimation stands around something like 22-25. Any kind of bank that deals with SME can work with us. Since Bangladesh Bank is pushing to release more loans to SMEs, many new banks are being interested to tap into that territory. So the possibility of more collaboration is one the rise.

Do you think banks are too harsh when it comes to giving loans to SMEs? Especially the “stringent” conditions they impose.

That used to be the case. Nevertheless, things are easing up now.

Do you work with startups? A lot of them are looking forward to venture capital (VC) for financing.

We can only offer services that the regulators allow us to. Under that frame work, we cannot really diversify to new areas without their permission. But in future we may venture into that area too. Right at the moment, we would like to focus on SMEs, though many of these companies are reluctant to be rated. There are two reasons. There is a price tag attached to it and they don’t see any benefit associated with the rating. But we try to make them understand the bright side of it. SMEs, in general, lack in documentation, i.e. accounts, book keeping, cash flow structure maintenance, etc. We help them become more structured. They also get to see the picture black and white, when the report is finally prepared by us. So we are trying to reach out to them.

Are you doing any kind of promotion to raise awareness? Do you have a social media promotion?

We are promoting through social media like facebook and LinkedIn. We are also in touch with the training institutes who are dealing with SMEs and startups. We conduct sessions and describe to them how they can get our services and what are the benefits associated with it. Our next target is to get associated with business associations. Through them, we would like to raise awareness among SMEs to get rated.

Are you happy with the growth of BDRAL?

The competition among the eight rating agencies in Bangladesh is stiff. We are the last to get the license though we were the third applicant. When we received the license, we were in the impression that we would get some sort of exclusivity, i.e. only we would rate SMEs. Later we found out that was quite not the scenario. There are other fully licensed rating agencies, who are also rating SMEs. That sort of put us under a tight competition. Nevertheless, we are working very hard. Besides, the pricing is another issue. We wanted to charge less to encourage more SMEs to take up our service. The minimum charge we fixed was Tk 8,500 which is a very low price for this kind of service. However, I am optimistic that better days are ahead. Hopefully, we can expand our business portfolio and perform better.