The Chinese Economic bubble burst triggering widespread panic in the global economy.

By Sheahan Nasir Bhuiyan

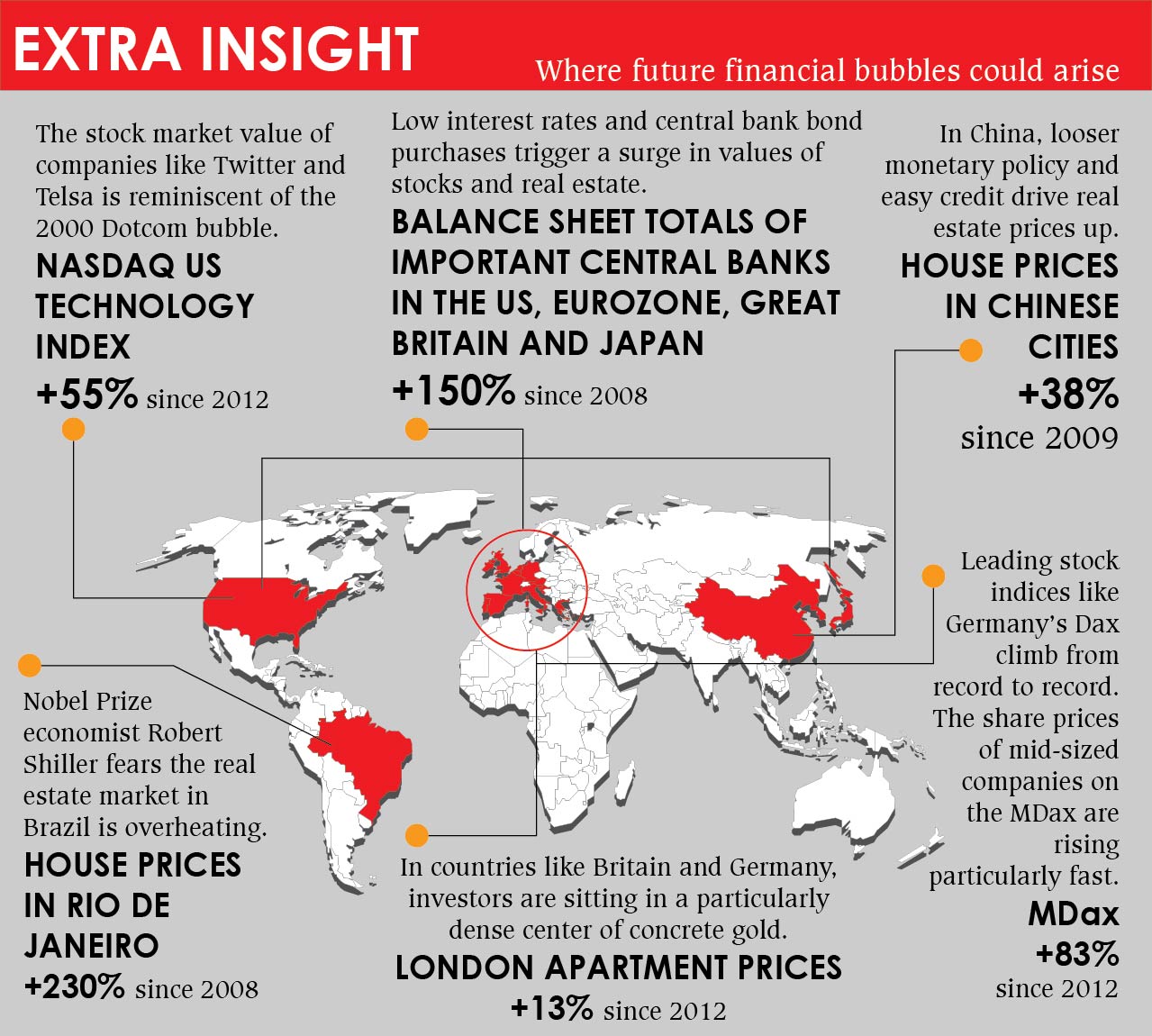

On Monday, August 24th 2015, China, the world’s second biggest economy, faced one of its biggest stock market crises. Stock prices were down by 8.5% at the Shanghai Composite index, the biggest single day drop in the markets since 2007. China’s state owned media vehicle, The People’s Daily, used the term “Black Monday” to describe the day’s events. Comparisons were drawn by some against some of the worst stock market crashes in the world. The drop wiped out whatever gains the market has made throughout the year. The current richest man in Asia, Wang Jianlin alone suffered losses of approximately $13 billion as a result of this crash. The effects were also felt far and away with most markets opening at much lower levels. The DAX in Germany was down by more than 20% since its peak. The Nikkei Index in Japan rolled down by 4.6% while The Dow experienced losses of about 4%. Apart from stocks, currencies in emerging markets have tumbled down. Commodities were not safe either, with Brent crude, the benchmark for oil prices worldwide, trading below $45 a barrel for the first time in six years. Even the price of gold, considered to be a safe commodity during times of economic hardships, has taken a hit. At that point the only stable assets were government bonds issued by the likes of the United States and Germany.

Markets have since recovered some of their losses amidst deep concerns regarding China’s economy. After all, it is the second biggest in the world, accounting for 15% of global GDP and contributes around half of global growth. The actual nature of the Chinese economy has been thrown into the limelight. Many analysts have long been questioning the official growth rate posted by the Chinese Government and the crash goes to show their skepticism may be well-founded. Furthermore, China’s large investments in developing economies, especially in Africa, has prompted fears that a economic meltdown in China will lead to downturns in those economies as well.

In order to understand this crash, we must go back to August 11th. The Chinese Government made a surprise announcement to devalue their national currency, the Yuan, which set off a chain of events, ultimately resulting in the market crash of August 24th. In the process, it is estimated that a total of $5 trillion has been wiped out from global stock prices. The devaluation was accompanied by a national agenda to increase participation in the stock market with the government encouraging citizens to invest in shares, funnelling a significant amount of funding into stocks. The Government intervened heavily by cutting interest rates to record lows, encouraging brokerage to buy billions of stocks and stopping the issuance of new shares to drive up current prices. Surprisingly, this rally came at a time when reports showed that the Chinese economy was slowing down. Despite the Government’s efforts, the weakened currency, along with rising investments and falling economic growth has created a bubble which burst on “Black Monday”, triggering widespread panic in the global economy.

However, it is important to note that the Chinese economy is very different from its Western counterparts and although this incident has revealed its potential weaknesses, it will be a mistake to expect similar consequences as those faced during the events that set off the global recession in 2008. China places far more importance in their property market than the stock market unlike Western economies. Properties account for up to a quarter of GDP and in the past few months, the market has shown good signs after going through a patchy phase. Despite encouragement from the government, only 5% of household wealth is tied up in stocks compared to nearly a third in the U.S. Moreover, stocks represent a very small portion of financing in Chinese companies as debts and bank loans provide most of the investments required. A stock market crash therefore, does not mean a loss in financing activities.

With such little wealth tied up in stock markets, the crash had minor impact amongst citizens. Very few ordinary Chinese will experience severe losses from this crash, just like very few people benefit from a market boom. This bodes well for the economy as China is reliant on its retail shoppers, and their spending has not decreased after the market crash. Tim Cook, on hearing about the market crash, has proclaimed that Apple has experienced strong growth throughout July and August in China. The fact that many Chinese are snapping up Apple products despite the market crash should allay any fears of a potential economic downturn.

Not that this means all is well in the long run though. China still faces a multitude of issues which may haunt them in the future. Part of the problem lies in the fact that there are many disputes between the numbers released by the government and the numbers estimated by analysts. The growth rate posted by the government of 7% is laughable according to sceptics, who place is at a more modest 2-3%. Debt has been claimed to be at nearly 250% of GDP and the working age group is slowly shrinking. Many analysts claim that China would eventually have to resort to free-market interventions to fix these issues but based on the Government’s interventions mentioned earlier, it seems unlikely. Despite their claims of introducing more free market reforms, especially after the market crash, it seems the Government is very reluctant to relinquish its control.

What does all this mean for Bangladesh? Trade between the two nations reached $8.6 billion in 2014, although it is heavily skewered towards the Chinese side. China provides 29% of Bangladesh’s total imports while exports amounted to only 1.7% of the total. This scenario is unlikely to change anytime in the near future, especially after the crash. China will want to increase its exports further to combat its falling growth rate. At the same time, imports will likely remain unchanged as the crash has not resulted in a reduced demand for consumer products and Bangladesh mostly exports garments and leather products to China. However, rising labor costs in China are slowly shifting the volume of garments trade over to Bangladesh. If this trend continues, it is very likely that Bangladesh may start enjoying higher exports to China.