Insights into the growth of the pharmaceutical industry of Bangladesh.

In 1972 the Bangladesh Association of Pharmaceuticals Industries (BAPI) was founded with 23 pharmaceutical businesses. BAPI is the only registered and recognised private-sector pharmaceutical association in the country and has 149 members. In addition, BAPI is a member of the International Federation of Pharmaceutical Manufacturers Association (IFPMA), which is located in Geneva, further solidifying its position in the private sector pharmaceuticals sphere.

The first companies to enter the pharmaceutical market sphere in the nation were Opsonin Pharma Ltd which had its beginnings in 1956, Square Pharmaceuticals Limited founded in 1958, Renata Limited which started operations as Pfizer (Bangladesh) in 1972, and Beximco Pharmaceuticals Ltd, as a subsidiary of Beximco Group, in 1976. These local companies still hold more than 90% of the market share.

MANUFACTURING

Pharmaceutical Manufacturing in Bangladesh comes in two main stages. The first stage involves Active Pharmaceutical Ingredient (API) manufacturing which makes the core components of every finished drug product and the second stage involves the production of the final drug. At this stage, the APIs are mixed with excipients, or inactive substances, which are then put into consumable form factors, for example, pills, tablets, and solutions.

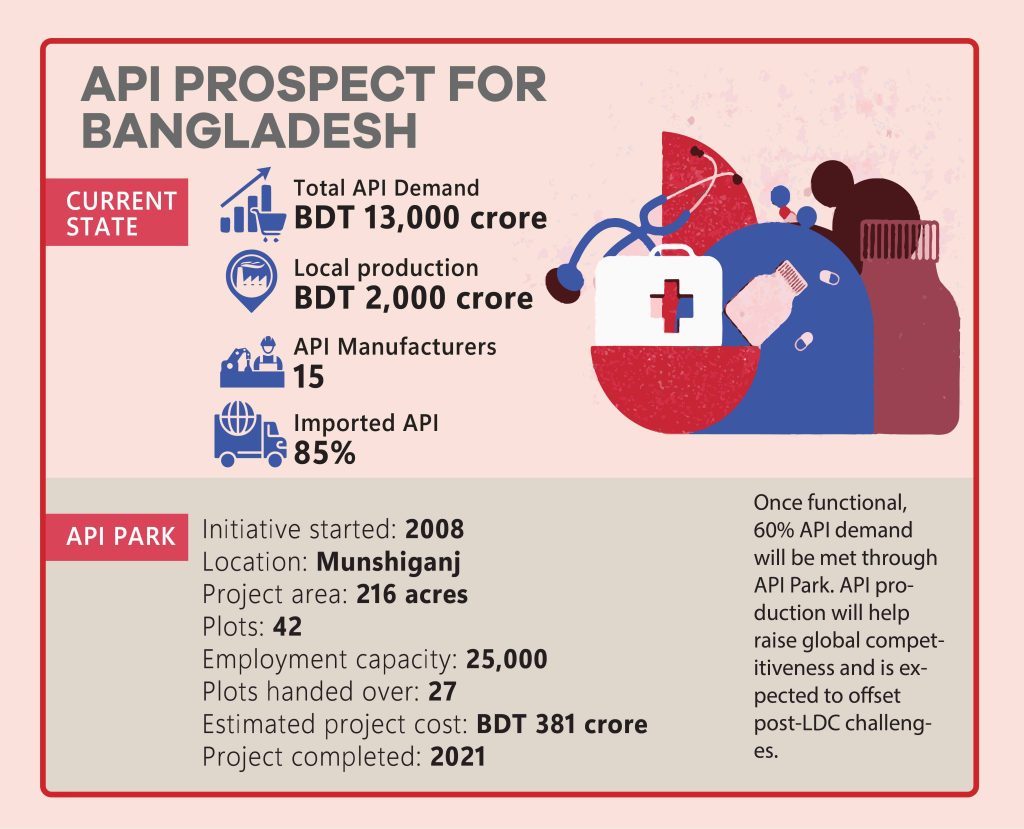

API Production

Bangladesh at the moment meets 98% of all its demand locally. However, it has to import nearly 85% of all the raw materials needed to make the APIs and the finished drug products. This heavy reliance on imports comes with its own challenges as fluctuating exchange rates and supply chain disruptions can make the market very volatile.

In order to support the production of APIs, the government has taken up various initiatives to meet the rising demand, this involves inaugurating a new API industrial park to allow pharmaceuticals to focus solely on API production. This is expected to help pharmaceutical companies gain a competitive edge not only in the local market but on the global scale as well as it could significantly lower import costs.

Medicine

The domestic pharmaceutical industry is valued at over BDT 27,000 crore and is estimated to grow 3 fold by 2030. This rise in demand is supported by the rise in the ageing population followed by the increased dependency on medications as well as the rise of healthcare in Bangladesh. Gastric, cardiovascular, respiratory, nervous system and oncological drugs have seen the highest growth among others. At the moment, local manufacturers dominate the market with a share of more than 90%, compared to 10% held by multinationals.

DISTRIBUTION

Despite having strong manufacturing and production numbers, medicines in Bangladesh are not as accessible and available to the general population. Determining the scale of this problem is a challenge in itself as there is very limited data on the factors that contribute to the low availability. The most recent systematic effort to assess medicine access in Bangladesh was the Bangladesh Health Facility Survey (2014), which collected data on the availability of 14 important medicines in public and private facilities. This survey discovered significant differences in the accessibility of various medications across public facility types, with some medications being made available to less than 10% of all facilities, such as amitriptyline, and others being almost exclusively in the private sector, for example, simvastatin/atorvastatin. Based on an assessment of the available limited data, it was also discovered that half of the physicians in the country working at public hospitals from district to union sub-centre levels were dissatisfied with the availability of medicines that were stocked in their facilities. Private-sector medicine tends to hold a higher inventory and therefore, ends up taking precedence over public-sector medicine. As a result, if the private sector decides to surge the prices of their stock of medicines, it becomes a burden on citizens to be able to afford it. Unaffordability denies patients access to these medicines. Furthermore, qualitative analysis has shown that the lack of demand for the public health service sector could be due to poor consumer experience stemming from health providers’ rude behaviours, misconduct, and poor quality of service.

IMPORT/EXPORT

As of 2023, Bangladesh’s pharmaceutical industry remains largely shielded from outside competition thanks to import restrictions on medications that are identical to those produced locally. Bangladesh is allowed to reverse-engineer patented generic pharmaceutical items in order to sell them domestically and export them to markets all over the world under the Trade-Related Aspects of Intellectual Property Rights (TRIPS) agreement of the World Trade Organisation (WTO). Bangladesh exports pharmaceutical products to 151 countries, including those in the EU, Africa and Latin America as well as the US, after catering to 98% of the domestic demand, according to BAPI. Bangladesh mainly exports medicine related to malaria, tuberculosis, cancer, leprosy, kidney dialysis, homoeopathy, biochemicals, Ayurvedic, and hydrocele alongside penicillin, streptomycin and anti-hepatic ones. As Bangladesh produces 97% of all its medicines internally, there are no significant imports of other medicines in the country.

However, Bangladesh imported USD 46.5 billion worth of API into the country in the year 2019. Most of these API imports of bulk drugs and intermediaries come from China, South Korea and India. This is because there is a lack of APIs in Bangladesh which is essential to decreasing the costs of raw materials. This also exposes Bangladesh to supply chain disruptions and price fluctuations.